Key Business Points

- The new Insurance Act 2025 eliminates credit purchases and requires full premium payment before coverage begins, but its annual payment structure may limit accessibility for most Malawians.

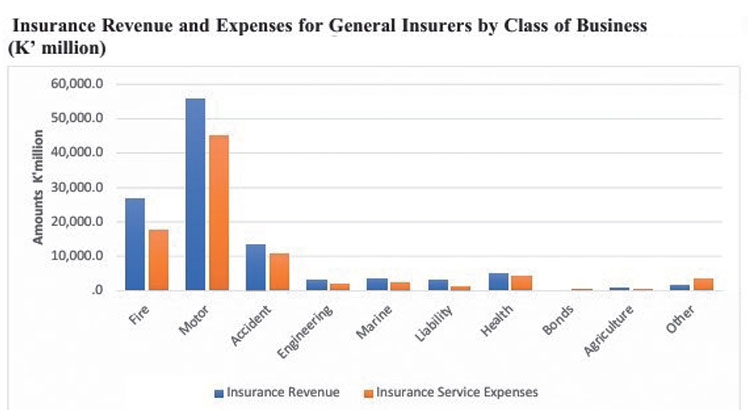

- Insurance uptake in Malawi remains under three percent, driven in part by mandatory motor third-party cover rather than voluntary participation.

- Banks are introducing premium financing to allow monthly instalment payments, offering a potential workaround to the upfront cost barrier.

Malawi’s general insurance sector faces a pivotal moment as the April 30 compliance deadline for the new Insurance Act approaches. The Consumers Association of Malawi (Cama) has raised concerns that the law’s strict "no premium, no cover" principle, while improving solvency safeguards, could unintentionally stifle broader insurance adoption by making policies unaffordable for most Malawians.

Under the new regime, insurance policies take effect only after the full annual premium is paid upfront—a shift from the previous practice that allowed credit arrangements. Cama executive director John Kapito argues that this structure clashes with the financial realities of many low and medium-income earners, who would find it easier to budget monthly or quarterly instalments rather than a lump-sum annual cost. He points out that insurance uptake is already low, largely confined to motor third-party cover due to legal requirements, and warns that demanding full payment at once could further deter voluntary participation. Kapito also notes that most Malawians are unfamiliar with insurance products and lack awareness of their benefits, compounding the impact of the high upfront costs.

Insurance industry representatives, however, defend the annual payment model as a globally recognised standard for managing risk and ensuring solvency. Dorothy Chapeyama, chairperson of the Insurance Association of Malawi, explains that insurers assume the full risk from the moment a policy starts and need secure funding in advance. She argues that the payment structure is not the main barrier—pointing instead to low disposable incomes, limited financial literacy and misconceptions about the value of insurance. Monthly payment options already exist for some corporate clients but come with higher administrative costs and risks such as policy lapses, which could undermine long-term sustainability.

Insurance expert Abdul Mageed Dyton echoes the industry’s stance, emphasising that insurers must cover total risk immediately upon policy inception. He highlights that commercial banks are now stepping in with premium financing solutions, allowing customers to spread their annual premium over 12 monthly instalments. Under these arrangements, banks pay insurers upfront and collect repayments from policyholders, making cover more accessible without imposing the additional burden on insurers.

Meanwhile, the Reserve Bank of Malawi’s Financial Stability Report shows the sector remains resilient in many respects, with capital rising 39.2 percent to K73.9 billion and a strong 45.4 percent solvency ratio. Yet liquidity pressures and exposure risks continue to weigh on the industry as it adjusts to regulatory change.

The debate underscores a broader challenge for Malawi’s insurance market: balancing prudent risk management with the need to expand reach and affordability. Options such as bank-backed premium financing could provide part of the solution, but lasting growth will likely depend on improved public awareness, flexible payment models tailored to local incomes, and clear communication of insurance’s role in protecting individuals and businesses from financial shocks.

What are your thoughts on this business development? Share your insights and remember to follow us on Facebook and Twitter for the latest Malawi business news and opportunities. Visit us daily for comprehensive coverage of Malawi’s business landscape.

- Malawi’s $20m Escom Investment: Reliable Energy Driving Business Growth and Stability - July 27, 2026

- Malawian Firm Launches Nasdaq IPO to Fund Lake Chilwa Development - July 27, 2026

- Kayelekera Returns to Production This August - July 25, 2026