From Hand to Mouth to Purchasing Power: Growing Malawi Businesses Through Household Demand

Key Business Points

- Improve household income – Target policies that raise wages, especially for rural workers, to reduce the 40 % of rural families whose earnings cannot meet basic needs.

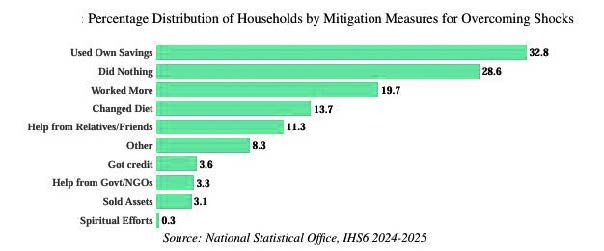

- Invest in savings and credit – Expand affordable micro‑credit and savings products so that more than 3 % of households can build a financial cushion.

- Accelerate growth – Lift the national growth rate above 10 % to achieve the lower‑middle income target for 2030 and turn current gains into real living‑standard improvements.

The latest Sixth Integrated Household Survey released by the National Statistical Office paints a stark picture for Malawi’s business community. Only 3.6 % of households reported having enough income to save for the future, while 41.3 % manage just enough to cover daily expenses. A quarter of families—25.4 %—must borrow to survive, leaving nearly two‑thirds without a safety net. Seventy‑five percent of families see themselves as poor or very poor, a figure that underscores the urgency for economic reform.

Rural households are hit hardest: 40.4 % report insufficient income, compared with 45.3 % in urban areas. Even amid a modest average growth of 2.2 %—well below the 10.6 % rate the World Bank estimates is needed to move Malawi from low to lower‑middle income—businesses feel the squeeze. High food prices (86.4 %) and costly inputs (73.6 %) strain profit margins, while drought affects nearly half of households.

Economists Agness Nyirongo of the Centre for Social Concern and economist Velli Nyirongo both warn that the real issue is not unemployment but low and unstable incomes, weak savings capacity, and a lack of protection against shocks. “Savings provide security during difficult times and create opportunities for investment,” Nyirongo stresses. She calls for bold interventions to lift household earnings and build resilience.

Milward Tobias, a former economic aide and presidential candidate, highlights a governance deficit. “The gap is in the lack of decisive and capable leadership to implement what is already available,” he says. Policymakers have designed measures to raise wages, reduce inflation, and support agriculture, but implementation has slipped.

For the private sector, this snapshot offers several actionable insights:

- Supply Chain Diversification – With food and input prices volatile, companies can explore local sourcing, contract farming, and agribusiness partnerships that reduce dependence on imported inputs.

- Micro‑Finance and Savings Platforms – Integrate mobile money and community savings schemes to help households build emergency funds. This not only improves consumer purchasing power but also expands the customer base for small retailers.

- Productivity‑Boosting Technologies – Invest in irrigation, drought‑tolerant crops, and digital tools that increase yields and lower input costs. Higher productivity translates into higher wages and stronger local demand for goods and services.

Chichewa‑speaking entrepreneurs can use these findings to tailor marketing. African markets value zokambirana kulimbikira (resilience) and community support. Messaging that highlights how a product or service helps families save, earn, or protect against shocks can resonate with consumers who are acutely aware of their financial fragility.

Policy reforms that spur real growth will also open new markets. If the government can achieve a 10 % growth trajectory by boosting manufacturing, improving infrastructure, and easing regulatory hurdles, the resulting rise in disposable income will fuel demand for everything from household appliances to digital services. This, in turn, will create ripple effects across supply chains, labour markets, and investment flows.

In sum, Malawi’s current household statistics reveal a society on the edge of shock and an economy that must pivot to channel growth into real wage gains. For businesses, the pathway to success lies in aligning product offerings and services with the needs of households that are barely able to survive day to day. By focusing on income‑elevating strategies, strengthening savings habits, and supporting resilient, technology‑enabled production, entrepreneurs can not only secure profit but also contribute to a more stable, prosperous Malawi.

What are your thoughts on this business development? Share your insights and remember to follow us on Facebook and Twitter for the latest Malawi business news and opportunities. Visit us daily for comprehensive coverage of Malawi’s business landscape.

-

MRA’s Kalondola Initiative Drives Economic Growth and Tax Revenue Surge

- August 11, 2026 - MCD urged to tap commodities for market growth – The Times Group - August 11, 2026

- Currency Shifts Cost K12bn: Business Impact Revealed - August 10, 2026